One Big Beautiful Bill Act: What It Means for CPA Firm Tax Season

Summary

The One Big Beautiful Bill Act (OBBBA) represents the most significant tax legislation since the Tax Cuts and Jobs Act of 2017, with sweeping changes to individual rates, business deductions, SALT caps, and new credits affecting virtually every CPA firm’s client base.

Key Takeaways

• The One Big Beautiful Bill Act (OBBBA) represents the most significant tax legislation since the Tax Cuts and Jobs Act of 2017. It makes sweeping changes to individual rates, business deductions, SALT caps, and new credits. These affect virtually every CPA firm’s client base.

• Individual impacts include modified tax bracket structures, updated standard deduction amounts, child tax credit parameter changes, and SALT deduction cap modifications. These require updated planning conversations for every client who itemises.

• Business impacts span revised rate structures, modified Section 199A QBI deductions, updated depreciation schedules, expanded R&D credits, and new energy incentives. They create both compliance complexity and advisory opportunities.

• CPA firms must update tax software configurations, preparation checklists, engagement letters, planning templates, and staff training materials before OBBBA-affected returns enter the workflow — a massive operational undertaking.

• The compliance workload surge is precisely where offshore teams provide maximum value — absorbing additional preparation work at $8–$35/hour while partners focus on high-value client advisory.

The One Big Beautiful Bill Act is here, and it changes everything for tax season planning. This is the most comprehensive tax legislation since the Tax Cuts and Jobs Act of 2017. It touches individual rates, business deductions, state and local tax treatment, new credits, and sunset provisions that affect virtually every client in every CPA firm’s portfolio.

The Joint Committee on Taxation has published detailed revenue estimates. The IRS is working to update forms, instructions, and processing systems. The AICPA Tax Section has issued practitioner guidance, and every major tax software vendor — Wolters Kluwer (CCH), Thomson Reuters (UltraTax), Intuit (Lacerte) — is racing to implement the changes.

For CPA firm partners and tax managers, OBBBA creates a dual challenge. The first is understanding the legislation thoroughly enough to advise clients accurately and identify planning opportunities. The second is simultaneously updating every operational element of your practice — software settings, preparation checklists, engagement letters, planning templates, and staff training — to reflect the new law before it affects filed returns.

The firms that navigate this smoothly will separate the two kinds of work. Advisory work (requiring partner expertise and client relationships) is distinct from operational compliance work (requiring thoroughness, accuracy, and capacity). That separation is exactly what offshore teams through Acculink CPA enable — and it’s never been more critical than during a major legislative transition year.

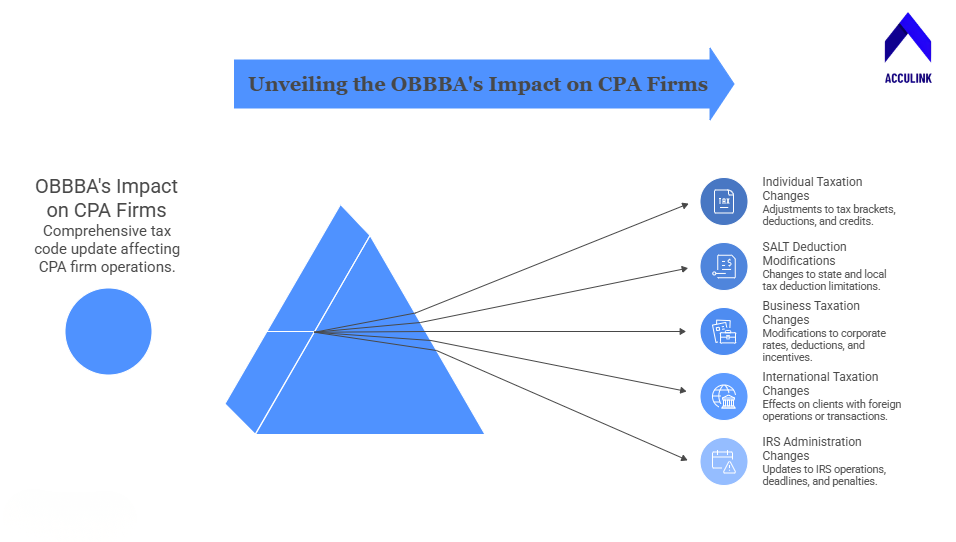

Key Provisions of the OBBBA

The One Big Beautiful Bill Act contains hundreds of provisions spanning individual taxation, business taxation, energy policy, international tax, and IRS administration. Here are the categories most relevant to CPA firm operations and client advisory. The analysis draws on the Joint Committee on Taxation and Congressional Research Service.

On the individual side, the legislation makes significant changes to tax bracket structures. It adjusts thresholds and rates affecting liability calculations at virtually every income level. Standard deduction amounts have been modified. That impacts the itemisation versus standard deduction calculus for millions of taxpayers. Child tax credit parameters have been updated — credit amounts, phase-out thresholds, and refundability provisions — affecting family tax planning conversations at every income bracket.

The SALT deduction cap — one of the TCJA’s most contentious provisions — has been modified under OBBBA. Changes to the state and local tax deduction limitation disproportionately affect clients in high-tax states. They require updated planning analysis for anyone who itemises and pays significant state income or property taxes. CPA firms in New York, New Jersey, California, Connecticut, and Illinois will see particularly high advisory demand around SALT changes.

On the business side, OBBBA modifies corporate rate structures, updates Section 199A qualified business income deduction parameters for pass-through entities, and revises depreciation schedules and cost recovery provisions. It also expands R&D credit provisions, introduces new energy-related incentives, and modifies various business deduction limitations. Each change requires updated preparation procedures, software configurations, and planning analysis for firms handling S corporation returns, partnership filings, and corporate returns.

International provisions affect firms with clients who have foreign operations or cross-border transactions. Administrative provisions affect IRS operations, filing deadlines, and penalty structures. Together, OBBBA creates the most comprehensive update to the tax code that practitioners have navigated since 2017 — and every CPA firm must prepare for its impact across the full client portfolio.

What Changes for Individual Clients

Individual tax provisions require CPA firms to update their approach to virtually every individual engagement, creating both compliance complexity and advisory revenue opportunities.

Tax bracket adjustments affect liability calculations at every income level. Prior-year estimates and planning projections need recalculation. Withholding recommendations may need adjustment, and quarterly estimated tax payments should be reviewed for adequacy. Firms should proactively communicate bracket changes and offer updated planning projections. Focus on clients with variable income, significant capital gains, or retirement distribution planning needs.

Standard deduction changes alter the itemisation threshold analysis. Some clients previously itemising may find the standard deduction more favourable under OBBBA; others may shift to itemising. This requires client-by-client analysis, adding time to every individual tax return engagement.

Child tax credit modifications affect family planning significantly. Changes to credit amounts, income phase-out thresholds, and refundability provisions require updated guidance and adjusted estimated tax calculations. The Congressional Budget Office estimates these provisions affect tens of millions of families. That means most CPA firms will have substantial numbers of affected clients.

SALT cap modifications deserve particular attention. Any change affects the itemisation calculus, pass-through entity tax election analysis, and geographic relocation considerations. Advisory conversations about SALT impacts are high-value engagements that partners should prioritise — and they’re only possible when partners have time freed from compliance preparation work.

Retirement provisions may include modifications to contribution limits, distribution rules, or RMD parameters affecting retirement planning conversations. Each provision change adds layers to every individual engagement. That compounds the per-return workload increase that OBBBA creates for CPA firm teams.

What Changes for Business Clients

Business provisions create both compliance complexity and advisory opportunities across every entity type CPA firms serve, from sole proprietors to complex multi-entity structures.

Corporate rate structure changes affect C corporations directly and flow through to entity election analysis. Updated rates may change the optimal structure for businesses choosing between C-corp, S-corp, and partnership formats. Firms should proactively review entity structures with business clients to ensure continued optimisation.

Section 199A qualified business income deduction changes affect every pass-through entity — partnerships, S corporations, and sole proprietors. Any modification to QBI calculation, limitation thresholds, or specified service restrictions requires updated preparation procedures for a large portion of most firms’ client bases. This is among the most technically complex areas of individual-business intersection taxation.

Depreciation and cost recovery changes affect capital investment planning. Updated schedules for bonus depreciation, Section 179 expensing, and recovery periods require recalculated depreciation projections. Firms providing virtual CFO advisory should proactively contact business clients with capital expenditure plans.

R&D credit expansion creates advisory opportunities for qualifying clients. Expanded provisions may bring new clients into eligibility or increase available credits — firms with R&D expertise should treat OBBBA as a business development trigger.

Energy incentives create advisory opportunities and compliance complexity for clients investing in efficiency, renewables, or electric vehicle infrastructure. The Department of Energy guidance on qualifying investments will be essential reference material for practitioners advising affected clients.

For firms handling business returns through offshore tax preparation teams, the key is ensuring offshore preparers receive the same OBBBA training as domestic staff. Acculink CPA’s professionals receive ongoing U.S. tax law training covering legislative changes, ensuring they’re prepared for OBBBA-affected returns from day one.

How to Update Your Tax Prep Workflow

Operational changes required for OBBBA implementation are substantial and should be planned systematically, not addressed reactively as issues arise during filing season. The AICPA has published implementation guidance that practitioners should review alongside vendor-specific updates.

Software configuration updates are the priority. Your tax software vendor will release OBBBA updates that need installation, testing, and verification against known scenarios before live client use. Assign a team member to monitor vendor communications from Thomson Reuters, Wolters Kluwer, or Intuit. They should coordinate updates and run test returns through updated software.

Preparation checklists must be updated for every affected return type. Individual checklists need new items for bracket analysis, SALT assessment, credit verification, and new-provision screening. Business checklists need items for entity structure review, QBI updates, depreciation verification, and credit eligibility. Share updated checklists with your offshore preparation team simultaneously.

Engagement letters may need revision reflecting new services, updated fee structures for additional OBBBA complexity, and communication about changed provisions. Consider sending proactive client communications summarising relevant OBBBA provisions — this serves both client service and business development purposes.

Staff training is essential for every preparer, reviewer, and client-facing professional. This includes offshore team members who prepare returns — they need identical training on new provisions, updated procedures, and modified checklists. Acculink CPA’s offshore professionals receive U.S. tax law update training as part of ongoing professional development through the company’s in-house L&D program.

Planning templates and projection models need OBBBA parameter updates before the planning season. Updated templates should be ready before client conversations begin, so projections use accurate figures from the start. For firms providing FP&A advisory, this is particularly time-sensitive.

Offshore Teams: Handling the OBBBA Compliance Surge

Major tax legislation always creates a compliance workload surge that tests every CPA firm’s capacity. OBBBA is no exception — and for many firms, the surge arrives on top of existing staffing gaps created by the accounting talent crisis that the profession has faced for years.

The surge manifests in three compounding ways. First, every return takes longer to prepare. Preparers must evaluate new provisions, apply updated calculations, and verify software implementation of the new law. A return that took 4 hours last year may take 5–6 hours this year — and additional time compounds across hundreds or thousands of returns.

Second, the review takes longer. Reviewers must verify the correct application of new provisions, check for missed opportunities under OBBBA’s new credits and deductions, and ensure prior-year assumptions have been updated. Review note volume typically increases in the first year of major legislation.

Third, client communication volume surges. Clients have questions about how OBBBA affects them, what has changed, and what planning actions to take. These conversations are valuable advisory opportunities billed at $300–$500/hour — but only if partners have time for them, rather than being consumed by preparation backlogs.

Offshore teams through Acculink CPA absorb the preparation workload surge, creating the capacity your partners need for advisory conversations. A dedicated offshore tax preparer trained on OBBBA provisions handles the additional preparation time at $8–$35/hour instead of the domestic equivalent cost. Five offshore preparers handling the volume increase save your firm $200,000+ during the transition period. They maintain filing capacity.

Acculink CPA provides pre-vetted, U.S.-trained tax professionals available within 5–7 days. They work in your software (CCH, UltraTax, Lacerte, Drake), follow your preparation procedures, and receive training on legislative changes, including OBBBA. During a legislative transition year, this additional capacity isn’t a luxury — it’s the difference between managing the surge and falling behind on client deliverables.

For a deeper look at how firms structure their offshore tax teams, see our guide on hiring offshore tax preparers and review the year-end accounting preparation strategies that complement OBBBA transition planning.

Frequently Asked Questions

When do OBBBA provisions take effect?

Most provisions take effect for tax years beginning after the bill’s enactment date. Some have delayed effective dates or phase-in periods. Check your tax software vendor and IRS guidance for specific provision timing.

Do I need to update client engagement letters?

Yes. Review and update engagement letters to reflect scope changes, additional OBBBA complexity, and fee adjustments. Consider adding proactive client communications about key provisions using AI drafting tools to accelerate the process.

Can offshore preparers handle OBBBA-related returns?

Yes. Offshore professionals at Acculink CPA receive training on U.S. tax law changes, including OBBBA provisions. They work on your software, follow your updated checklists, and adapt to new requirements alongside your domestic team.

How much additional work does OBBBA create per return?

Firms typically report 15–30% additional preparation time per return in the first filing season under major legislation. The additional time decreases as teams gain experience. Offshore capacity absorbs this increase without straining your domestic staff.

Should I hire extra staff for the OBBBA season?

Offshore staffing provides the most flexible additional capacity. Hire dedicated preparers at $8–$35/hour with no long-term commitment, rather than domestic hires at $55,000–$80,000+ annual salary for what may be a transitional workload peak.

Where can I find a detailed OBBBA analysis?

The Joint Committee on Taxation, Congressional Research Service, AICPA Tax Section, and your tax software vendor all publish detailed provision-by-provision analysis. Your firm’s offshore team can help compile and organise this research.

References

Joint Committee on Taxation — Joint Committee on Taxation

Congressional Research Service — Congressional Research Service reports

IRS — Internal Revenue Service (IRS)

American Institute of CPAs (AICPA) — American Institute of CPAs (AICPA)

IRC Section 199A — Cornell Law — IRC §199A — qualified business income deduction

Congressional Budget Office — Congressional Budget Office

Thomson Reuters Tax & Accounting — Thomson Reuters Tax & Accounting

Department of Energy — U.S. Department of Energy

About Acculink CPA

Acculink CPA is a premier offshore staffing and outsourcing company purpose-built for CPA firms, accounting firms, and tax firms in the United States, Canada, and the UAE. With a team of 300+ qualified professionals — including CPAs, Chartered Accountants, Enrolled Agents, and Big 4-trained staff — Acculink provides dedicated offshore accountants, bookkeepers, tax preparers, auditors, virtual CFOs, and virtual assistants at $8–$35/hr, delivering up to 75% cost savings compared to domestic hiring. The company is ISO 27001 certified, SOC 2 Type II aligned, IRS §7216 compliant, and GDPR compliant, with zero security breaches in 5+ years of operations. Acculink offers a 40-hour free trial with no setup fees, no recruitment charges, and no long-term contracts. Over 80 CPA firms across the United States trust Acculink to deliver quality, security, and scalability.

Website: Acculink CPA | Schedule a Call: book a 45-minute call | Email: Info@acculinkcpa.com | Phone: +1 (203) 997-0224

Tags:

About the Author

Related Posts

Hire Offshore Tax Preparers for CPA & Accounting Firms – Why Outsourced Tax Preparation Works Best.

How to hire an offshore tax preparer for your CPA firm — 1040/1065/1120/1120-S, CCH/UltraTax/Drake, IRS §7216-…

Payroll Outsourcing Services for CPA & Accounting Firms – Your Guide to Payroll & Compliance

How payroll outsourcing keeps CPA firms' clients compliant — 941/940 and multi-state filings, W-2/1099, on a 2…

Sales Tax Compliance Outsourcing for CPA & Accounting Firms – Why It Works

How outsourcing sales tax compliance handles nexus, multi-state filings, and exemption certificates for CPA fi…