The 2026 CPA Exam Changes: Impact on Firm Hiring and the Talent Pipeline

Summary

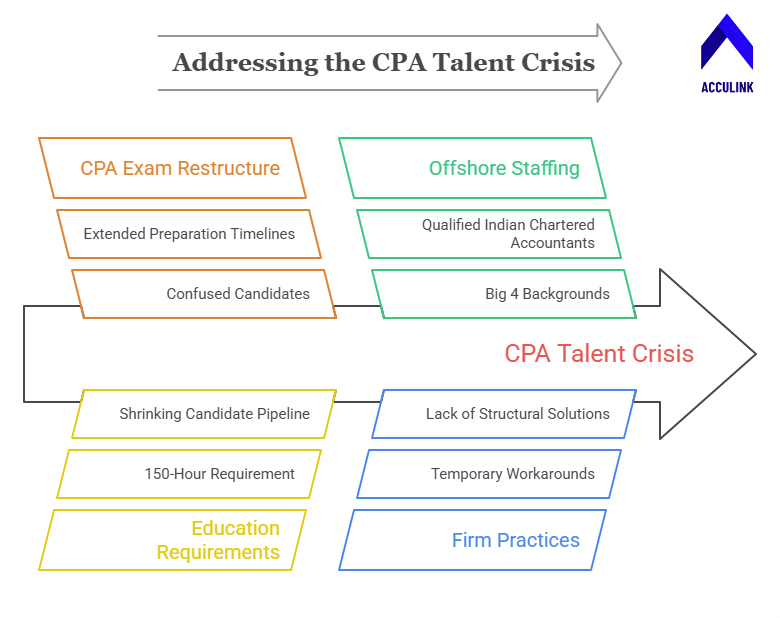

The CPA exam underwent a major restructure in 2024, replacing the traditional four-section format with a core-plus-discipline model that has extended preparation timelines, confused candidates, and contributed to declining pass rates across all sections.

The 2026 CPA Exam Changes: Impact on Firm Hiring and the Talent Pipeline

Key Takeaways

• The CPA exam underwent a major restructure in 2024, replacing the traditional four-section format with a core-plus-discipline model. The new format has extended preparation timelines, confused candidates, and contributed to declining pass rates across all sections.

• Fewer candidates are sitting for the exam, and those who do are passing at lower rates — compounding the talent crisis the AICPA has documented for years, leaving CPA firms chronically understaffed at every experience level.

• The 150-hour education requirement continues to discourage accounting graduates from pursuing CPA licensure. Meanwhile, NASBA data shows the candidate pipeline shrinking year over year with no near-term reversal in sight.

• Indian Chartered Accountants available through offshore staffing providers hold qualifications from the ICAI (10–15% pass rate) that are arguably more selective than the U.S. CPA exam, with many bringing Big 4 backgrounds and years of U.S. tax experience.

• Offshore staffing is not a temporary workaround — it’s a structural solution to a structural talent problem that the CPA exam changes are making worse, available through Acculink CPA at $8–$35/hour with a 40-hour free trial.

The CPA exam has always been a barrier to entry for the accounting profession — that’s by design. A rigorous licensing exam ensures only qualified professionals earn the right to sign audits, prepare complex tax returns, and advise clients on financial matters. The public interest demands high standards, and the CPA exam has historically delivered them.

But what happens when the barrier becomes so high, so complex, and so time-consuming that it discourages qualified candidates from even attempting it? That’s the question the profession is confronting in 2026, as the restructured CPA exam’s impact on the talent pipeline becomes impossible to ignore.

The American Institute of CPAs and the National Association of State Boards of Accountancy implemented a significant restructure beginning in 2024. The changes were intended to modernise the exam, reflect the evolving nature of practice, and allow candidates to demonstrate specialised knowledge. The intentions were sound. The consequences for the talent pipeline — and for every CPA firm trying to hire qualified professionals — have been deeply concerning.

The Journal of Accountancy and Accounting Today have covered the pipeline crisis extensively. They document how fewer graduates are entering accounting programs, fewer are pursuing CPA licensure, and those who do face a more complex exam with lower initial pass rates. For CPA firm partners and managers, this translates directly into longer hiring timelines, higher salary demands, and persistent capacity gaps. These constrain growth and threaten client service quality.

This blog examines what changed in the CPA exam, how those changes are affecting pass rates and candidate volume, and what the downstream impact means for firm hiring. It also covers why Indian Chartered Accountants available through offshore providers represent a compelling structural solution, and the exact steps to build offshore capacity that insulates your firm from domestic talent market volatility.

What Changed in the CPA Exam

The CPA exam restructure replaced the traditional four-section format — Auditing and Attestation (AUD), Business Environment and Concepts (BEC), Financial Accounting and Reporting (FAR), and Regulation (REG) — with a new core-plus-discipline model that fundamentally changes how candidates prepare for and complete the licensing examination.

Under the new structure, candidates must pass three core sections: AUD, FAR, and REG (with expanded content from the former BEC integrated into these cores). Then, candidates choose one of three discipline sections: Business Analysis and Reporting (BAR), Information Systems and Controls (ISC), or Tax Compliance and Planning (TCP). Each discipline tests specialised knowledge at a deeper level than core sections cover.

The AICPA positioned this as an evolution reflecting how modern CPAs work in increasingly specialised environments. The exam should test both foundational knowledge and deeper competency in a chosen area. The rationale was sound from a professional standards perspective.

The practical impact on candidates has been significant across multiple dimensions. First, preparation timelines have extended. Candidates still pass four sections, but discipline sections require studying material not covered by the traditional exam — meaning existing study materials, review courses, and preparation strategies need to be completely rebuilt. Early cohorts under the new format reported feeling substantially underprepared. The reason was that CPA review providers and practice exams hadn’t fully calibrated to new content expectations.

Second, the unfamiliarity factor suppressed early pass rates. Any exam format change creates a transition period where candidates and preparation providers are still calibrating. The 2024–2025 cohorts bore the brunt of this adjustment. Pass rate data published by NASBA reflected the uncertainty with noticeable declines across multiple sections.

Third, the 18-month rolling window for passing all four sections creates compounding pressure. If a candidate passes three sections but fails the fourth, they risk losing credit for earlier sections as the window expires — a demoralising outcome documented by the Journal of Accountancy as causing some candidates to abandon the process entirely rather than restart the cycle.

For CPA firms, the exam changes mean that the pipeline of newly licensed CPAs entering the profession is narrower than it was before the restructure — at a time when firms were already struggling to hire. Every firm relying exclusively on domestic CPA talent is competing for a shrinking pool. Firms that have built offshore accounting teams have insulated themselves from the domestic supply constraint.

The Impact on Pass Rates and Candidate Volume

The numbers tell a sobering story for anyone who depends on a steady flow of new CPAs entering the profession. Both candidate volume and pass rates are trending in the wrong direction.

CPA exam pass rates, which had been trending in the mid-to-high 40% range for most sections in recent years, declined across the board. The drop followed the restructure. The discipline sections — being entirely new in format, content, and testing approach — saw particularly variable results during initial testing windows. NASBA data showed some discipline sections reporting pass rates in the low 40s initially, significantly below historical averages. While some stabilisation has occurred as review courses improved, pass rates remain below pre-restructure levels for most sections.

Candidate volume has been declining independently of the exam restructure. The drivers are converging factors that the Bureau of Labour Statistics and AICPA have documented extensively. The 150-hour education requirement adds an extra year of schooling beyond a bachelor’s degree, creating both a financial burden (additional tuition, lost income) and an opportunity cost. Graduates see peers in technology and finance earning higher starting salaries without additional certification requirements.

Rising student debt makes the additional year of education increasingly painful to justify. Competition from technology, finance, and consulting career paths that offer higher starting compensation without certification hurdles also hurts. It siphons talented graduates away from accounting before they ever sit for the exam. And the perception that the CPA credential’s return on investment is diminishing relative to cost and effort further depresses candidate interest.

The exam restructure added another layer of discouragement on top of these structural trends. Candidates planning preparation under the old format faced the choice of rushing to complete before the transition or restarting under the new format. Some chose neither. New candidates face a more complex exam with less mature study resources and lower reported pass rates — hardly an encouraging environment.

The cumulative effect is a shrinking funnel with fewer entrants and lower throughput. Fewer accounting graduates pursue the CPA. Fewer CPA candidates pass the exam. Fewer new CPAs enter the profession each year. For CPA firms that need qualified professionals to prepare individual tax returns, conduct audits, handle S corporation filings, and serve clients, this matters. The pipeline contraction is the defining workforce challenge of the decade — and the exam changes are making it worse.

What This Means for CPA Firm Hiring

The practical impact on CPA firm hiring is severe, worsening, and affecting firms of every size across every service area and geographic market.

Recruiting timelines have extended dramatically. Firms that filled a tax preparer or staff accountant position in 4–8 weeks five years ago now report timelines of 3–6 months. Candidates with CPA credentials or CPA-eligible status command premium salaries and field multiple competing offers simultaneously. Accounting Today salary surveys show entry-level accountant salaries rising 15–25% over three years. Experienced tax professionals and audit managers are seeing even larger increases.

The quality of available candidates has shifted noticeably. Firms increasingly hire candidates without CPA credentials who may never pursue licensure — accounting graduates meeting the 120-hour bachelor’s requirement but not the 150-hour CPA eligibility threshold. These professionals handle bookkeeping, tax preparation, and financial statement work capably. But they cannot sign audit reports or represent clients before the IRS in the same capacity as licensed CPAs.

Geographic distribution of talent is increasingly uneven. Major metropolitan areas still attract accounting graduates, but firms in smaller cities and suburban areas face acute shortages. Remote work only partially addresses them.

Tax season staffing has become particularly painful. The seasonal nature of tax work means firms need maximum capacity during January through April — exactly when every other firm is competing for the same limited talent pool. Domestic temporary tax staffing agencies have raised rates substantially ($35–75/hour). Quality also varies dramatically. Some firms have simply accepted reduced capacity, turning away work or extending deadlines — sacrificing revenue and client relationships.

The CPA exam changes exacerbate every one of these trends by reducing the flow of new CPAs into the profession. Each year, fewer candidates pass, which means the cumulative talent deficit grows deeper. Domestic hiring alone cannot fill this structural gap. Firms need a different talent strategy — one that accesses qualified professionals outside the constrained domestic pipeline.

How Indian Chartered Accountants and EAs Fill the Gap

Here’s where the conversation shifts from problem to solution — and where most firm owners discover an option they hadn’t seriously considered or didn’t know existed at the quality level now available.

India’s Chartered Accountant (CA) program, administered by the Institute of Chartered Accountants of India (ICAI), is one of the most rigorous professional accounting certifications in the world. The CA exam has a pass rate of approximately 10–15% — significantly more selective than the U.S. CPA exam’s 45–50% pass rate. Candidates who earn the CA designation have demonstrated mastery of accounting principles, taxation, auditing, financial management, and corporate law. The multi-stage examination process typically takes 3–5 years of intensive study and practical training.

Many Indian CAs also hold additional qualifications that specifically prepare them for U.S. work: MBA degrees from top Indian business schools, and internationally recognised ACCA certifications. Others hold U.S. Enrolled Agent credentials that qualify them specifically for U.S. tax preparation and IRS representation. A significant number have direct experience with U.S. tax preparation through positions at Big 4 firms’ Indian offices — Deloitte, PwC, EY, and KPMG all have substantial Indian operations serving U.S. clients — or through offshore staffing companies that exclusively serve American CPA firms.

These professionals are trained on the same tax software that U.S. firms use daily. CCH Axcess, UltraTax CS, Lacerte, Drake, ProSystem fx — offshore professionals at providers like Acculink CPA work in these platforms every day. They understand U.S. tax forms, schedules, and IRS §7216 compliance requirements because that’s their entire professional focus. They communicate in English, operate during overlapping business hours (the Indian time zone creates a natural “second shift” for U.S. firms). They attend your team meetings, follow your review processes, and build institutional knowledge of your clients over time.

The qualification comparison is striking when you examine it objectively: a U.S. CPA candidate passes an exam with a 45–50% pass rate, while an Indian CA passes an exam with a 10–15% pass rate. Both credentials represent rigorous professional standards, but the Indian CA designation arguably reflects a more selective process. Add Big 4 training and years of U.S. engagement experience, and the offshore professionals available through Acculink CPA represent a strong talent pool. It is both deeper in technical capability and dramatically more cost-effective than the shrinking domestic CPA pipeline.

The cost differential makes the case even more compelling. An experienced offshore tax preparer through Acculink CPA costs $8–$35/hour fully loaded — no additional charges for benefits, office space, recruiting, or turnover replacement. A comparable domestic hire costs $55,000–$80,000+ in base salary before adding 25–35% for benefits, $5,000–12,000 for office space, $5,000–10,000 for recruiting, and the inevitable turnover replacement costs that the Bureau of Labour Statistics estimates at $15,000–40,000 per departure.

Offshore as the Structural Solution to the CPA Pipeline Crisis

The CPA talent pipeline is not going to fix itself in any timeframe that matters for your firm’s staffing needs this year, next year, or the year after. Even if the AICPA succeeds in reforming the 150-hour requirement, even if exam pass rates stabilise under the new format, and even if university accounting programs increase enrollment — all of which are uncertain outcomes on multi-year timelines — the cumulative talent deficit that has built over the past decade will take years to reverse.

Offshore staffing is not a temporary band-aid while the pipeline recovers. It’s a structural solution to a structural problem. The talent exists in India — in abundance, at high quality levels verified by rigorous ICAI certification, and at cost points that allow small and mid-size firms to compete effectively with larger firms and PE-backed competitors.

Consider the capacity math for a typical small firm with 10–15 domestic professionals. Adding 3–5 offshore team members through Acculink CPA effectively increases your firm’s total capacity by 20–35% while reducing your average cost per professional by 30–40%. Those offshore professionals handle the preparation and compliance work that currently consumes your domestic team’s time — tax return preparation, bookkeeping, financial statement drafting, audit workpaper preparation — freeing your licensed CPAs and experienced managers to focus on review, advisory, and client relationships.

The onboarding timeline comparison is dramatic. Acculink CPA provides pre-vetted professionals with documented qualifications and relevant experience. They are available to start within 5–7 days of engagement. Full onboarding typically completes in 2–3 weeks. Compare that to the 3–6 months required for a domestic accounting hire. Factor in job posting, resume screening, interviews, offer negotiation, notice period, and onboarding ramp-up.

The retention economics are equally favourable. Offshore providers manage the employment relationship, provide career development, and maintain backup staffing. If an offshore team member transitions, the provider handles replacement within 1–2 weeks with handover support — minimal disruption versus domestic turnover, where replacing an experienced accountant costs $15,000–$40,000 and creates months of productivity gaps.

The CPA exam changes have made a challenging talent situation measurably worse. Waiting for the pipeline to recover is not a viable business strategy. Building your firm’s capacity through offshore staffing is both an immediate solution and a long-term competitive advantage. It insulates your practice from domestic talent volatility, regardless of what happens with exam reform timelines.

Explore the approach that 80+ CPA firms across the United States have already adopted. See our existing blog on hiring offshore tax preparers for a detailed walkthrough of the hiring process, or review our compliance advisory guide to understand how IRS §7216 compliance works with offshore teams.

Frequently Asked Questions

Are the CPA exam changes permanent?

The core-plus-discipline format is the intended permanent structure. The AICPA may adjust content areas over time, but the fundamental restructure is not expected to be reversed. Firms should plan their hiring strategies assuming the new format persists.

Will fewer new CPAs mean my firm can’t grow?

Not if you diversify your talent sources. Offshore professionals with CA, EA, or equivalent qualifications handle the preparation and compliance work that CPAs traditionally performed. That allows your licensed CPAs to focus on review, advisory, and client service.

Are Indian CAs really comparable to U.S. CPAs?

The ICAI CA exam has pass rates of 10–15% versus 45–50% for the U.S. CPA exam. Many Indian CAs also hold EA credentials and have Big 4 experience with U.S. clients. They work in CCH Axcess, UltraTax, Lacerte, and Drake daily.

How quickly can I add offshore capacity?

Through Acculink CPA, pre-vetted professionals start within 5–7 days, fully onboarded in 2–3 weeks. Compare that to the 3–6 month domestic hiring timeline. Start with the 40-hour free trial to evaluate risk-free.

What about the 150-hour requirement debate?

Several states and the AICPA are exploring alternatives, including competency-based pathways. However, legislative changes take years to implement. Offshore staffing addresses the talent gap now, not in the uncertain future.

What roles can offshore professionals fill?

Tax preparation, tax review, bookkeeping, audit support, financial reporting, payroll, and virtual CFO support. Virtually any compliance or preparation role can be staffed offshore.

References

American Institute of CPAs (AICPA) — American Institute of CPAs (AICPA)

National Association of State Boards of Accountancy (NASBA) — National Association of State Boards of Accountancy (NASBA)

Institute of Chartered Accountants of India (ICAI) — Institute of Chartered Accountants of India (ICAI)

Journal of Accountancy — Journal of Accountancy

Accounting Today — Accounting Today

Bureau of Labour Statistics — U.S. Bureau of Labor Statistics

IRS Section 7216 Information Centre — IRS Section 7216 Information Center

Thomson Reuters Tax & Accounting — Thomson Reuters Tax & Accounting

About Acculink CPA

Acculink CPA is a premier offshore staffing and outsourcing company purpose-built for CPA firms, accounting firms, and tax firms in the United States, Canada, and the UAE. With a team of 300+ qualified professionals — including CPAs, Chartered Accountants, Enrolled Agents, and Big 4-trained staff — Acculink provides dedicated offshore accountants, bookkeepers, tax preparers, auditors, virtual CFOs, and virtual assistants at $8–$35/hr, delivering up to 75% cost savings compared to domestic hiring. The company is ISO 27001 certified, SOC 2 Type II aligned, IRS §7216 compliant, and GDPR compliant, with zero security breaches in 5+ years of operations. Acculink offers a 40-hour free trial with no setup fees, no recruitment charges, and no long-term contracts. Over 80 CPA firms across the United States trust Acculink to deliver quality, security, and scalability.

Website: Acculink CPA | Schedule a Call: book a 45-minute call | Email: Info@acculinkcpa.com | Phone: +1 (203) 997-0224

Tags:

About the Author

Related Posts

Hire Offshore Bookkeepers for CPA & Accounting Firms – Blueprint for Outsourced Bookkeeping

How to hire an offshore bookkeeper for your CPA firm — what they do, how vetting and onboarding work, cost (up…

Hire Offshore Accountants for CPA & Accounting Firms – Why Outsourced Accounting Works

How to hire an offshore accountant for your CPA firm — month-end close, GL, GAAP reporting, in your software —…

Best Accounting Practice Management Software for CPA Firms and Accounting Firms (2026)

For most accounting and CPA firms, TaxDome is the most popular all-in-one practice management platform, bundli…