How Tariffs and Trade Wars Are Impacting Accounting Firms and Their Clients in 2026

Summary

How Tariffs and Trade Wars Are Impacting Accounting Firms and Their Clients in 2026

Key Takeaways

-

The 2026 tariff landscape — shaped by IEEPA executive orders, Section 232 steel and aluminium duties, and Section 122 emergency tariffs — is directly impacting CPA firm clients across manufacturing, retail, agriculture, healthcare, and construction.

-

CPA firms are facing a surge in client questions about inventory costing, landed cost calculations, customs duties, import reclassification, and scenario planning for tariff-exposed supply chains.

-

The accounting treatment of tariffs requires careful application of ASC 330 (Inventory), ASC 450 (Contingencies), and revenue recognition guidance — creating advisory opportunities for firms with the expertise.

-

Firms that position themselves as tariff advisory resources will differentiate from compliance-only competitors — but advisory work requires capacity, which offshore teams can provide by handling the compliance workload.

-

Acculink CPA’s offshore accountants and virtual CFOs can handle the compliance and analytical work (landed cost calculations, inventory revaluation, scenario modelling) while partners focus on client advisory conversations.

If you’re a CPA firm partner in 2026, tariffs are no longer a background policy issue. They’re a front-page, client-facing, revenue-impacting reality that’s reshaping how your clients do business — and how your firm delivers value.

Since early 2025, a cascade of tariff actions has transformed the U.S. trade landscape. IEEPA-based executive orders imposing broad tariffs on Chinese imports, Section 232 duties on steel and aluminium from multiple countries, Section 122 emergency measures targeting specific industries, and retaliatory tariffs from trading partners have created a complex, fast-moving environment that clients are struggling to navigate.

Your clients aren’t calling to ask about tariff policy in the abstract. They’re calling because their cost of goods sold just jumped 15%, their supplier is passing through duty charges they didn’t budget for, their inventory valuation is changing mid-quarter, and they need to know how to account for all of it. They’re calling because they need their CPA firm to be more than a compliance shop — they need strategic advisory guidance.

This guide covers the 2026 tariff landscape, how tariffs affect CPA firm clients across industries, the accounting treatment of tariff-related costs, the advisory opportunities for firms that step up, and how offshore teams can provide the capacity to handle both compliance and advisory work simultaneously.

As the economist Milton Friedman once noted, “One of the great mistakes is to judge policies and programs by their intentions rather than their results.” For CPA firms, the results of tariff policy are landing on your clients’ financial statements right now. The question is whether your firm is positioned to help them navigate it.

The 2026 Tariff Landscape: What’s Changed

Understanding the current tariff environment is an essential context for advising clients. Here’s the landscape as of early 2026:

Under the International Emergency Economic Powers Act (IEEPA), the administration has imposed broad tariffs on Chinese imports across multiple product categories. These tariffs affect everything from electronics components and industrial machinery to consumer goods and raw materials. The cumulative effective tariff rate on many Chinese goods now exceeds 50% when layered with existing Section 301 tariffs from prior administrations.

For CPA firms, the practical impact is immediate: clients who import from China are seeing their cost of goods sold jump dramatically, and they need help quantifying the impact, adjusting their financial projections, and evaluating whether to absorb the cost, pass it through, or restructure their supply chains.

Section 232 Steel and Aluminium Duties

Section 232 tariffs on steel (25%) and aluminium (10%) have been expanded to include additional countries and product subcategories. These duties directly impact manufacturing, construction, automotive, and infrastructure clients. Secondary effects ripple through supply chains as domestic steel prices rise in response to reduced import competition.

The downstream effects are significant. A construction company that doesn’t import steel directly still faces higher costs because its domestic steel suppliers have raised prices to match the tariff-protected market. CPA firms need to help clients understand both the direct and indirect cost impacts.

Section 122 Emergency Tariffs

In a less common move, the administration has invoked Section 122 of the Trade Act to impose temporary emergency tariffs on specific product categories to address balance-of-payments concerns. These tariffs are time-limited (up to 150 days without Congressional approval) but have created uncertainty for importers who don’t know whether the measures will be extended, expanded, or allowed to expire.

The accounting challenge here is the uncertainty itself. Clients need to plan for multiple scenarios: the tariff continues, the tariff expires, or the tariff is replaced with something different. This requires the kind of scenario modelling that CPA firms with advisory capabilities are well-positioned to deliver.

Retaliatory Tariffs from Trading Partners

Canada, the EU, and other trading partners have imposed retaliatory tariffs on U.S. exports. This creates a double impact for CPA firm clients with international operations: higher input costs from U.S. tariffs on imports, and reduced export competitiveness from retaliatory duties on their products abroad. Agricultural exporters and manufacturers with significant international sales are being squeezed from both sides.

How Tariffs Affect CPA Firm Clients: Industry-by-Industry Impact

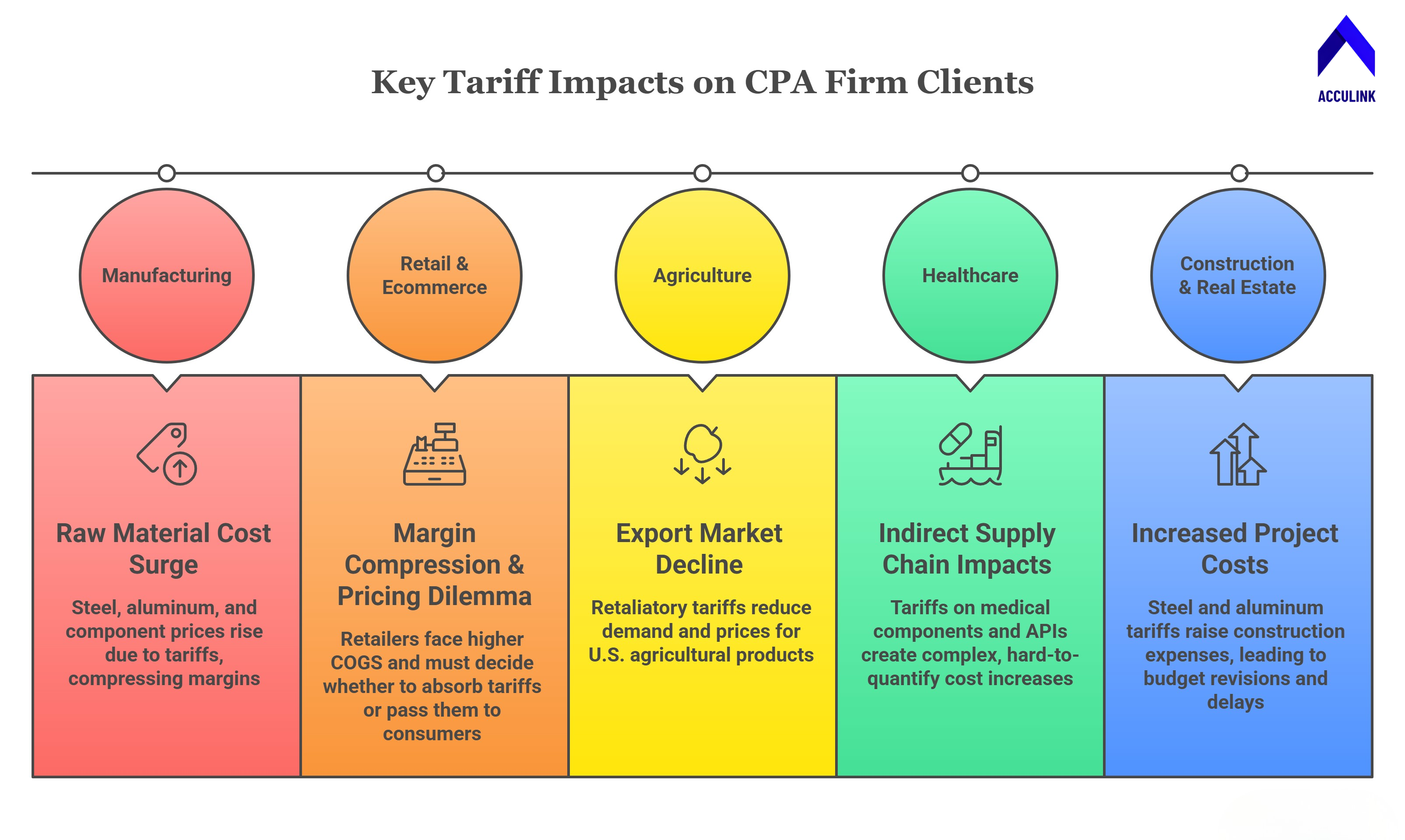

Manufacturing

Manufacturers are the hardest hit. Raw material costs (steel, aluminium, components from China) have surged, compressing margins. Clients face immediate questions: How do we account for tariff costs in inventory valuation? Should we reclassify imported components to lower-duty HTS codes? Can we restructure supply chains to source from non-tariffed countries? What’s the break-even point for reshoring production?

CPA firms serving manufacturers need to help with landed cost recalculations, inventory revaluation under ASC 330, and scenario modelling for alternative sourcing strategies. The complexity multiplies for manufacturers with multiple product lines sourced from different countries — each product line may face different tariff rates, different supplier alternatives, and different pricing constraints. For more on serving this industry, see Acculink’s manufacturing accounting services.

Retail and E-commerce

Retailers — especially those sourcing consumer goods from China — face margin compression as tariff costs flow through to cost of goods sold. The pricing decision is brutal: absorb the tariff cost and accept lower margins, or pass it through to consumers and risk losing volume. CPA firms are being asked to model both scenarios and advise on pricing strategy, promotion timing, and inventory purchasing acceleration. E-commerce businesses face an additional layer of complexity. Many online sellers source products from multiple countries through dropshipping or third-party logistics providers, making it difficult to track which products are tariff-exposed and which are not. CPA firms that can help clients build inventory tracking systems that capture tariff costs at the SKU level will deliver significant value. For industry-specific guidance, see Acculink’s e-commerce accounting and outsourcing

Retaliatory tariffs from China, Canada, and the EU are hammering U.S. agricultural exporters. Soybean, pork, dairy, and grain exporters face reduced demand and lower prices in key export markets. CPA firms serving agricultural clients need to help with revenue forecasting under reduced export scenarios, government subsidy accounting (trade adjustment payments), and crop insurance claims.

The seasonality of agriculture makes this even more challenging. Farmers make planting decisions months before harvest, and tariff changes during the growing season can dramatically alter the economics of crops already in the ground. CPA firms need to help agricultural clients build flexible financial plans that account for tariff volatility. For industry-specific insights, see Acculink’s agriculture accounting page.

Healthcare

Medical device manufacturers and pharmaceutical companies face tariffs on imported components, active pharmaceutical ingredients (APIs), and packaging materials. The healthcare industry’s complex supply chains mean tariff impacts are often indirect and difficult to quantify. CPA firms need to help clients trace tariff costs through multi-tier supply chains and assess the impact on product-level profitability. For firms serving healthcare clients, see Acculink’s healthcare accounting services.

Construction and Real Estate

Steel and aluminium tariffs directly increase construction costs for commercial, residential, and infrastructure projects. Developers are revising project budgets, delaying starts, and renegotiating contracts. CPA firms serving real estate clients face questions about capitalisation of tariff-related cost overruns, contract modification accounting, and project feasibility analysis. For more, see Acculink’s real estate accounting services.

Accounting for Tariffs: Technical Guidance for CPA Firms

The accounting treatment of tariff costs requires careful application of existing GAAP guidance. Here are the key areas:

Inventory Costing (ASC 330)

Under ASC 330, inventory is measured at the lower of cost or net realisable value. Tariff costs — import duties, customs fees, and related charges — are part of the cost of inventory when they are incurred to bring inventory to its current condition and location. This means tariff costs should be included in landed cost calculations and allocated to inventory, not expensed immediately.

However, if tariff-driven cost increases push total inventory cost above net realisable value (because the client can’t pass the full cost through to customers), inventory write-downs may be required. This is a judgment call that requires understanding the client’s pricing power and market conditions. CPA firms should document the NRV analysis thoroughly, including the assumptions about future selling prices and disposal costs.

Contingency Assessment (ASC 450)

For tariffs that are subject to ongoing legal challenges, retroactive adjustments, or policy uncertainty (like Section 122 tariffs that may expire), CPA firms need to assess whether a contingent loss or gain exists. If a tariff refund or reduction is probable and estimable, it may be appropriate to recognise a receivable. If additional tariff exposure is probable (e.g., from reclassification risk), a liability or disclosure may be required.

The key challenge is determining probability. Tariff policy is inherently political and unpredictable. CPA firms should generally take a conservative approach: recognise contingent losses when probable and estimable, but don’t recognise contingent gains (such as expected tariff reductions) until they are virtually certain.

Revenue Recognition Implications

For clients with long-term contracts that include cost-adjustment clauses, tariff cost increases may trigger contract modifications under ASC 606. CPA firms need to evaluate whether tariff costs are passed through under existing contract terms, represent a separate performance obligation, or require contract modification accounting. This is particularly relevant for construction contractors, government contractors, and manufacturers with multi-year supply agreements.

Income Tax Implications

Tariffs are customs duties — they’re not income taxes. But tariff costs affect pre-tax income, which affects income tax calculations. Additionally, some tariff mitigation strategies (like accelerating depreciation on reshored equipment under Section 179 or bonus depreciation) have income tax implications that require integrated planning. CPA firms should coordinate tariff advisory with tax planning and advisory services to ensure clients receive holistic guidance.

Financial Statement Disclosure

Significant tariff exposure may require disclosure in financial statement notes, particularly for audited or reviewed statements. CPA firms should evaluate whether tariff risks constitute a significant risk and uncertainty under ASC 275, whether subsequent events (tariff changes after the balance sheet date) require disclosure, and whether tariff impacts on going concern assessments need to be addressed. Proper disclosure protects both the client and the firm.

The Advisory Opportunity: How CPA Firms Can Add Value

Tariff disruption created an advisory opportunity. Clients don’t just need their books updated — they need strategic guidance. Here’s where CPA firms can step up:

Scenario Modelling and Sensitivity Analysis

Build financial models showing the impact of different tariff scenarios on client profitability. What happens if tariffs increase by other 10%? What if retaliatory tariffs expand to new product categories? What’s the breakeven point for reshoring vs. continuing to import? This is classic virtual CFO and FP&A work — and it’s exactly the kind of analysis offshore professionals can prepare for partner review.

Supply Chain Cost Analysis

Help clients map their supply chains, identify tariff-exposed nodes, and quantify the total cost impact, including direct duties, freight changes, and indirect effects. Compare the total landed cost of current suppliers against alternative sources in non-tariffed countries. This analysis often reveals that the cheapest supplier before tariffs is no longer the cheapest supplier after tariffs — creating an opening for supply chain restructuring that permanently reduces costs.

Pricing Strategy Advisory

Work with clients to model pricing strategies: full pass-through, partial absorption, selective product repricing, and bundled pricing approaches. Each strategy has different margins, volumes, and competitive implications that clients need quantified, not just discussed. Offshore analysts can build the pricing models; partners can present the strategic recommendations.

HTS Code Optimisation

Harmonised Tariff Schedule (HTS) classification determines the duty rate. In many cases, products can be legitimately classified under alternative HTS codes with lower duty rates. CPA firms can work with customs brokers to review client classifications and identify savings opportunities. This is compliance work — but with direct bottom-line impact that clients value and will pay advisory fees for.

Tariff Mitigation Strategies

Advise clients on tariff mitigation options: Foreign Trade Zones (FTZs), duty drawback programs, bonded warehouses, first-sale valuation, and temporary importation under bond (TIB). Each strategy has accounting, compliance, and operational implications that CPA firms are well-positioned to navigate. Many clients are unaware that these programs exist — proactive education builds trust and positions your firm as a strategic advisor.

How Offshore Teams Help CPA Firms Handle the Tariff Workload

Here’s the operational reality: tariff advisory work is time-intensive. The analysis, modelling, inventory revaluation, and financial statement adjustments all require skilled professionals. But your partners can’t do advisory work if they’re buried in compliance deliverables.

This is where offshore teams become essential. Acculink CPA’s offshore accountants, virtual CFOs, and FP&A professionals can handle the following:

-

Landed cost recalculations: Updating inventory costing models to include new tariff rates, freight changes, and customs fees across all product lines and supplier relationships.

-

Inventory revaluation workpapers: Preparing lower-of-cost-or-NRV analyses under ASC 330 for tariff-impacted inventory, including documentation of key assumptions and judgments.

-

Scenario modelling: Building Excel-based financial models showing the impact of various tariff scenarios on client P&L, cash flow, and margins — with sensitivity tables that partners can walk clients through.

-

Management reporting: Producing tariff impact dashboards and management reports that partners can present to clients during advisory meetings.

-

Tax return adjustments: Incorporating tariff-related cost changes into tax return preparation, including Section 199A calculations affected by changed COGS.

-

Bookkeeping and reconciliation: Keeping the day-to-day accounting and bookkeeping running smoothly while partners focus on advisory conversations with clients.

The model works like this: offshore professionals handle the analytical and compliance work overnight (from the U.S. perspective). By morning, partners have scenario models, revaluation workpapers, and updated financials ready for client meetings. Partners focus entirely on interpreting results, advising clients, and building relationships — the activities that drive firm growth and justify advisory fees.

What CPA Firms Should Do Right Now

If your firm hasn’t yet built a tariff advisory capability, here’s a practical action plan:

Step 1: Identify Tariff-Exposed Clients

Review your client base and identify every client with import-dependent supply chains, export exposure to retaliatory-tariff markets, or significant raw material costs tied to tariffed commodities (steel, aluminium, Chinese components). Prioritise outreach to these clients — they’re already feeling the impact and will value proactive communication from their CPA firm.

Step 2: Develop Tariff Advisory Templates

Create standardised templates for landed cost analysis, inventory revaluation, scenario modelling, and pricing impact assessment. These templates allow your team (including offshore staff) to produce consistent, professional deliverables efficiently. Standardised templates also make it easier to scale the advisory capability across your client base.

Step 3: Build Capacity with Offshore Support

If your team is already stretched, you can’t layer advisory work on top of existing compliance obligations without burning out your staff. Acculink CPA provides pre-vetted professionals who can ramp within 2–3 weeks — handling compliance work so your partners have time for advisory, or directly producing the analytical deliverables for partner review. Start with a 40-hour free trial to evaluate fit.

Step 4: Proactively Reach Out to Clients

Don’t wait for clients to call you. Proactive outreach demonstrates expertise and builds trust. Send a targeted email or schedule a call with tariff-exposed clients offering a complimentary tariff impact assessment. The firms that reach out first will capture the advisory engagement; the firms that wait will be seen as reactive.

Step 5: Monitor Policy Developments

The tariff landscape is changing monthly. Assign someone on your team to monitor developments from the Office of the U.S. Trade Representative, Customs and Border Protection, and trade policy news sources. Update clients proactively when changes affect their business. This ongoing monitoring builds your firm’s reputation as a trusted advisory resource.

Frequently Asked Questions

How do tariffs affect accounting for CPA firm clients?

Tariffs increase the landed cost of imported goods, requiring updates to inventory valuation under ASC 330, potential write-downs if costs exceed net realisable value, adjustments to cost of goods sold, and revised financial projections. They also create advisory opportunities in scenario modelling, pricing strategy, and supply chain optimisation.

What is the accounting treatment for tariff costs?

Tariff costs (import duties, customs fees) are included in the cost of inventory under ASC 330 as costs necessary to bring inventory to its current condition and location. They are not expensed immediately unless the inventory is for immediate sale and the tariff cost is incurred at the point of sale.

How can CPA firms help clients with tariff impacts?

CPA firms can provide landed cost analysis, inventory revaluation, scenario modelling for different tariff levels, pricing strategy advisory, HTS code optimisation, and guidance on tariff mitigation strategies like Foreign Trade Zones and duty drawback programs.

What industries are most affected by the 2026 tariffs?

Manufacturing, retail/ecommerce, agriculture, healthcare (medical devices and pharma), and construction/real estate are the most directly impacted. Any industry with significant import exposure or export dependence on retaliatory-tariff markets is affected.

How can offshore teams help with tariff-related accounting work?

Offshore professionals can handle landed cost calculations, inventory revaluation workpapers, scenario modelling, management reporting, bookkeeping adjustments, and tax return preparation — freeing partners to focus on client advisory conversations that drive revenue growth.

Do tariffs create advisory revenue opportunities for CPA firms?

Absolutely. Tariff disruption is one of the strongest advisory catalysts in 2026. Clients need scenario modelling, pricing strategy, supply chain analysis, and mitigation planning — all billable advisory services. Firms that build this capability early will capture revenue that compliance-only firms leave on the table.

References

Office of the U.S. Trade Representative — https://ustr.gov/

U.S. Customs and Border Protection — https://www.cbp.gov/

FASB ASC 330 — Inventory — https://asc.fasb.org/

American Institute of CPAs (AICPA) — https://www.aicpa.org/

About Acculink CPA

Acculink CPA is a premier offshore staffing and outsourcing company purpose-built for CPA firms, accounting firms, and tax firms in the United States, Canada, and the UAE. With a team of 300+ qualified professionals — including CPAs, Chartered Accountants, Enrolled Agents, and Big 4-trained staff — Acculink provides dedicated offshore accountants, bookkeepers, tax preparers, auditors, virtual CFOs, and virtual assistants at $8–$35/hr, delivering up to 75% cost savings compared to domestic hiring. The company is ISO 27001 certified, SOC 2 Type II aligned, IRS §7216 compliant, and GDPR compliant, with zero security breaches in 5+ years of operations. Acculink offers a 40-hour free trial with no setup fees, no recruitment charges, and no long-term contracts. Over 80 CPA firms across the United States trust Acculink to deliver quality, security, and scalability.

Website: Acculink CPA | Schedule a Call: book a 45-minute call | Email: Info@acculinkcpa.com | Phone: +1 (203) 997-0224

Tags:

About the Author

Related Posts

IRS 7216 Compliance for Offshore Tax Preparation: What Every CPA Firm Must Know

IRS Section 7216 is the federal regulation governing how tax return preparers can disclose and use taxpayer in…

Tax Season Survival Guide: How CPA Firms Use Offshore Teams to Handle Peak Workloads

Tax season capacity planning should start in September — not January. Firms that wait until the returns start …

Understanding the One Big Beautiful Bill Act: Tax Implications for CPA Firms and Their Clients

Understanding the One Big Beautiful Bill Act: Tax Implications for CPA Firms and Their Clients