Accounting for Cryptocurrency and Digital Assets: What CPA Firms Need to Know in 2026

Summary

Accounting for Cryptocurrency and Digital Assets: What CPA Firms Need to Know in 2026

The cryptocurrency tax landscape will continue to evolve as the IRS issues additional guidance, new legislation addresses digital assets, and the industry itself develops new transaction types. CPA firms that invest in crypto expertise today are building a practice area that will grow for years as digital asset adoption continues expanding across individual investors, businesses, trusts, and retirement accounts. The combination of specialised knowledge, dedicated software tools, and cost-effective offshore processing through Acculink CPA creates a scalable and profitable crypto tax practice that positions your firm as the go-to advisor for digital asset clients in your market. Every crypto client you serve well becomes a referral source within a community that actively shares professional recommendations.

The firms that dismiss crypto as a fad or a niche too small to pursue are making a strategic mistake. Digital assets are embedded in the financial system permanently, IRS enforcement is intensifying annually, and the clients holding crypto are precisely the high-value, financially engaged individuals and businesses that every CPA firm wants in its client base. Building crypto capability now, supported by offshore processing capacity that makes the volume economics work, is an investment in the future growth and relevance of your practice.

Common Crypto Tax Mistakes CPA Firms Must Avoid

Failing to Report All Taxable Events

Many taxpayers and some practitioners assume that only crypto-to-fiat conversions are taxable. In reality, every crypto-to-crypto trade is a taxable disposition. Trading Bitcoin for Ethereum, swapping tokens on a decentralised exchange, or using crypto to purchase an NFT all trigger capital gains calculations. CPA firms must ensure that all taxable events are captured, not just the obvious cash-out transactions.

Ignoring DeFi Transactions

DeFi activity, including providing liquidity, yield farming, and borrowing against crypto collateral, all create complex taxable events that are easy to overlook. Liquidity pool deposits may be treated as dispositions of the deposited tokens. Yield farming rewards are taxable income. Liquidation events in borrowing protocols created realised gains or losses. CPA firms must ask clients specifically about DeFi activity and use specialised software that tracks these transactions.

Using Incorrect Cost Basis Methods

Without proper tracking, the cost basis defaults to FIFO, which may not be optimal for the client. Specific identification can produce significantly better tax outcomes by allowing the client to select which lots to sell. However, specific identification requires contemporaneous documentation at the time of each sale. CPA firms should establish cost basis methodology with clients before transactions occur, not at tax time.

Not Accounting for Lost or Stolen Crypto

Clients who lost crypto to exchange hacks, wallet compromises, or scams may have deductible losses. However, the tax treatment of lost crypto is complex and depends on the circumstances. Theft losses for individuals were limited by TCJA but may be available for business taxpayers. CPA firms should document the loss circumstances thoroughly and apply the appropriate tax treatment based on the client-specific situation.

Key Takeaways

-

The IRS has significantly increased crypto enforcement in 2026, with mandatory digital asset questions on Form 1040, expanded broker reporting under the Infrastructure Investment and Jobs Act, and dedicated crypto audit teams.

-

CPA firms must understand the tax treatment of common crypto transactions: buying, selling, trading, staking, mining, DeFi yield farming, NFTs, airdrops, and forks.

-

Form 8949 reporting for digital assets requires cost basis tracking across potentially thousands of transactions — dedicated crypto tax software is essential.

-

Building a crypto tax practice is a significant growth opportunity for CPA firms, as crypto-active clients are actively seeking CPAs who understand digital assets.

-

Offshore tax preparers from Acculink CPA can handle the volume-intensive crypto transaction processing while partners focus on tax planning and advisory.

Cryptocurrency is no longer a niche asset class for tech enthusiasts. In 2026, digital assets are mainstream — held by individuals, businesses, trusts, and retirement accounts. The IRS has made digital asset taxation a top enforcement priority, with dedicated audit teams, expanded reporting requirements, and a mandatory question on every Form 1040 asking about digital asset transactions.

For CPA firms, this creates both a challenge and an opportunity. The challenge is that crypto accounting is complex, the rules are evolving, and many practitioners are unfamiliar with the specific tax treatment of staking, DeFi, NFTs, and other digital asset activities. The opportunity is that crypto-active clients are desperately seeking CPAs who understand their transactions — and they’re willing to pay premium fees for competent guidance.

This guide covers everything CPA firms need to know about cryptocurrency accounting in 2026: the IRS position, reporting requirements, tax treatment of common transactions, tools for crypto accounting, and how to build a crypto tax practice with offshore support from Acculink CPA.

The IRS Position on Crypto (2026 Update)

The IRS classifies cryptocurrency and digital assets as property for federal tax purposes. This means every sale, trade, or disposition of a digital asset is a taxable event subject to capital gains tax. The IRS has progressively tightened enforcement since 2019, and 2026 represents the most aggressive enforcement posture to date.

Key IRS positions include: all digital asset transactions are taxable events (buying goods with crypto, trading one token for another, selling for fiat currency), the digital asset question on Form 1040 must be answered by every taxpayer, crypto exchanges and brokers are required to issue Form 1099-DA (new in 2026) reporting gross proceeds from digital asset transactions, and the IRS has dedicated resources specifically to crypto audit and enforcement.

Crypto Tax Reporting Requirements

Form 8949 and Schedule D

Every sale or disposition of a digital asset must be reported on Form 8949 (Sales and Other Dispositions of Capital Assets) and summarised on Schedule D. This includes sales of cryptocurrency for fiat currency, trades of one cryptocurrency for another, using crypto to purchase goods or services, and conversions between crypto and stablecoins. For active traders with hundreds or thousands of transactions, Form 8949 can span dozens of pages. This is where volume-intensive processing from offshore tax preparers becomes invaluable.

Cost Basis Tracking

The most complex aspect of crypto tax compliance is cost basis tracking. When a taxpayer buys Bitcoin at different times and prices, sells a portion, the cost basis method (FIFO, LIFO, specific identification) determines the gain or loss. Clients who have used multiple exchanges, wallets, and DeFi protocols may have transaction histories spanning thousands of entries across dozens of platforms. Reconstructing this data for cost basis calculation requires specialised crypto tax software.

Tax Treatment of Common Crypto Transactions

Buying and Selling

Purchasing crypto with fiat currency is not a taxable event. Selling crypto for fiat is a taxable event, with gain or loss calculated as the difference between the sale price and the cost basis. Holding period determines short-term (ordinary income rates) vs long-term (preferential capital gains rates) treatment. The long-term threshold is one year.

Staking and Mining Income

Staking rewards and mining income are taxed as ordinary income at the fair market value on the date received. This creates a tax liability even if the tokens are not sold. The cost basis of the received tokens is the fair market value at receipt, which becomes the starting point for future capital gains calculations when the tokens are eventually sold.

DeFi Yield Farming and Liquidity Provision

DeFi transactions are among the most complex in crypto taxation. Providing liquidity to decentralised exchanges, yield farming, and borrowing against crypto collateral creates taxable events that the IRS has not fully addressed with specific guidance. CPA firms must apply general tax principles to novel transaction types — an area where experienced judgment is essential, al and AI tools fall short.

NFTs

Creating and selling NFTs generates ordinary income or capital gains depending on the creator’s status (hobby vs business). Purchasing and reselling NF follows standard capital asset rules. Royalty income from secondary NFT sales is ordinary income. The classification of NFTs as collectables (subject to the 28% maximum capital gains rate) vs standard capital assets remains an area of IRS focus.

Airdrops and Hard Forks

Tokens received through airdrops are taxable as ordinary income at fair market value on the date received. Hard fork tokens (where a blockchain splits into two) are taxable at the date the taxpayer has dominion and control over the new tokens. Cost basis of airdropped and forked tokens is the fair market value at receipt.

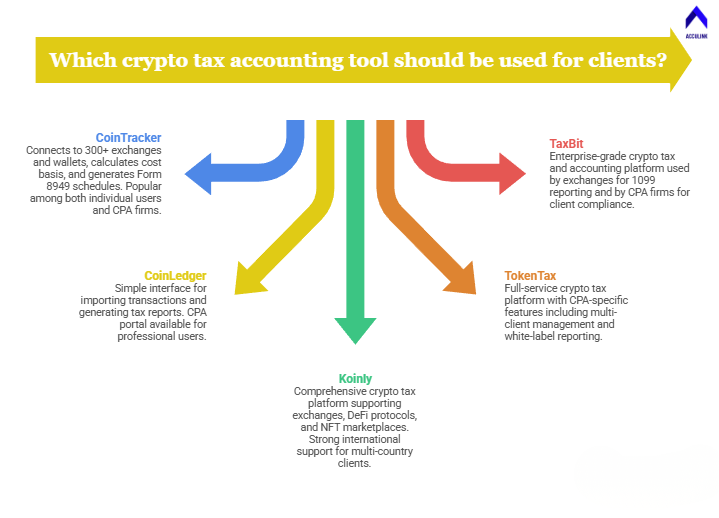

Tools for Crypto Tax Accounting

Manual tracking of crypto transactions is impractical for any client with significant activity. These specialised tools integrate with exchanges and wallets to automate transaction aggregation and tax reporting:

-

CoinTracker: Connects to 300+ exchanges and wallets, calculates cost basis, and generates Form 8949 schedules. Popular among both individual users and CPA firms.

-

CoinLedger (formerly CryptoTrader.Tax): Simple interface for importing transactions and generating tax reports. The CPA portal available for professional users.

-

Koinly: Comprehensive crypto tax platform supporting exchanges, DeFi protocols, and NFT marketplaces. Strong international support for multi-country clients.

-

TokenTax: Full-service crypto tax platform with CPA-specific features including multi-client management and white-label reporting.

-

TaxBit: Enterprise-grade crypto tax and accounting platform used by exchanges for 1099 reporting and by CPA firms for client compliance.

Building a Crypto Tax Practice

Crypto taxation is a significant niche opportunity for CPA firms in 2026. Here’s how to build a practice:

Develop Expertise

Invest in training on crypto tax rules, DeFi mechanics, and the evolving IRS guidance. The AICPA, state CPA societies, and specialised providers offer crypto-focused CPE courses. Follow IRS announcements and Treasury guidance closely.

Invest in Software

Choose one or two crypto tax platforms and develop proficiency. CoinTracker and Koinly offer the best balance of features and usability for CPA firms. The investment is modest ($500–$2,000/year for professional plans) compared to the fees crypto clients pay.

Market to Crypto Clients

Crypto clients actively seek CPAs who understand digital assets. Market your crypto expertise through your website, LinkedIn, local crypto meetups, and online communities. A dedicated crypto tax services page on your firm’s website signals expertise and attracts organic search traffic.

Use Offshore Support for Volume Processing

Crypto tax preparation is extremely volume-intensive. A single client with an active trading history may have thousands of transactions requiring reconciliation, cost basis calculation, and Form 8949 preparation. Offshore tax preparers from Acculink CPA handle this processing work efficiently while partners focus on tax planning strategies, advisory conversations, and complex judgment calls around novel transaction types.

How to Advise Crypto Clients

Beyond compliance, crypto clients need advisory guidance on tax-loss harvesting strategies to offset gains in volatile markets, timing of staking reward claims to manage ordinary income recognition, entity structuring for active traders considering business treatment under Section 475, gifting and charitable donation strategies using appreciated crypto, and estate planning for digital asset holdings, including access and custody planning.

These advisory conversations command premium fees and build deep client loyalty. The compliance work (Form 8949 preparation, cost basis tracking) can be handled by offshore teams, freeing your expertise for the high-value planning work.

Frequently Asked Questions

Is cryptocurrency taxable in the United States?

Yes. The IRS classifies cryptocurrency as property. Every sale, trade, or disposition is a taxable event. Staking, mining, and airdrop income are taxed as ordinary income at fair market value on receipt.

What forms do CPA firms use for crypto reporting?

Form 8949 for sales and dispositions, Schedule D for capital gains summary, Schedule 1 for staking and mining income, and Form 1099-DA (new in 2026) received from exchanges reporting gross proceeds.

What software should CPA firms use for crypto tax?

CoinTracker, Koinly, CoinLedger, TokenTax, and TaxBit are the leading options. Choose based on the number of clients, complexity of transactions (DeFi, NFTs), and integration with your existing tax software.

Can offshore teams handle crypto tax preparation?

Yes. Offshore tax preparers from Acculink CPA process crypto transaction data, calculate cost basis, prepare Form 8949 schedules, and integrate the results into the overall tax return. Partners review the work and handle advisory.

References

IRS Virtual Currency Guidance — https://www.irs.gov/businesses/small-businesses-self-employed/virtual-currencies

AICPA Digital Assets Resources — https://www.aicpa.org/

About Acculink CPA

Acculink CPA is a premier offshore staffing and outsourcing company purpose-built for CPA firms, accounting firms, and tax firms in the United States, Canada, and the UAE. With a team of 300+ qualified professionals — including CPAs, Chartered Accountants, Enrolled Agents, and Big 4-trained staff — Acculink provides dedicated offshore accountants, bookkeepers, tax preparers, auditors, virtual CFOs, and virtual assistants at $8–$35/hr, delivering up to 75% cost savings compared to domestic hiring. The company is ISO 27001 certified, SOC 2 Type II aligned, IRS §7216 compliant, and GDPR compliant, with zero security breaches in 5+ years of operations. Acculink offers a 40-hour free trial with no setup fees, no recruitment charges, and no long-term contracts. Over 80 CPA firms across the United States trust Acculink to deliver quality, security, and scalability.

Website: Acculink CPA | Schedule a Call: book a 45-minute call | Email: Info@acculinkcpa.com | Phone: +1 (203) 997-0224

Tags:

About the Author

Related Posts

Hire Offshore Tax Preparers for CPA & Accounting Firms – Why Outsourced Tax Preparation Works Best.

How to hire an offshore tax preparer for your CPA firm — 1040/1065/1120/1120-S, CCH/UltraTax/Drake, IRS §7216-…

Payroll Outsourcing Services for CPA & Accounting Firms – Your Guide to Payroll & Compliance

How payroll outsourcing keeps CPA firms' clients compliant — 941/940 and multi-state filings, W-2/1099, on a 2…

Sales Tax Compliance Outsourcing for CPA & Accounting Firms – Why It Works

How outsourcing sales tax compliance handles nexus, multi-state filings, and exemption certificates for CPA fi…